It’s hard to say which feels worse: owing money or being owed. Regardless of which of position you’re in, you want payments to be made as soon as possible, so you can settle invoices or generate revenue faster. In many cases — especially if the payor or payee is in a remote location — using Automated Clearing House (ACH) transactions is the quickest way to make it happen — and making it happen through the ACH network just got a lot faster.

In fact, ACH payment services are moving faster than ever, thanks to upgrades banks have made recently, pivotal changes that support a speedier Automated Clearing House (ACH) system — an electronic network that facilitates financial transactions in the U.S. and processes high-volume “batches” of credit and debit transactions that total trillions of dollars a year.

The ACH network was originally developed in the 1970s when it “seemed that the increasing volume of paper checks used by businesses and consumers to pay their bills would eventually exceed the ability of the existing computer systems to process and sort the checks efficiently,” according to the Federal Reserve Bank of New York.

Our Reliance on the ACH Network

The ACH network developers were right; a more efficient electronic payment processing network would eventually be necessary, as ACH transaction statistics from the National Automated Clearinghouse Association (NACHA) bear out.

In the 3rd quarter of 2016, ACH network transactions totaled 5,105,163,857 (not including on-us volume), up from 4,828,781,609 in the 3rd quarter of 2015 for a rise of 5.72%. The dollar volume differential for the same period is up 6.1%. In 3rd quarter 2016, roughly 11 trillion dollars passed through the ACH network — about 6% more than during the same quarter a year earlier.

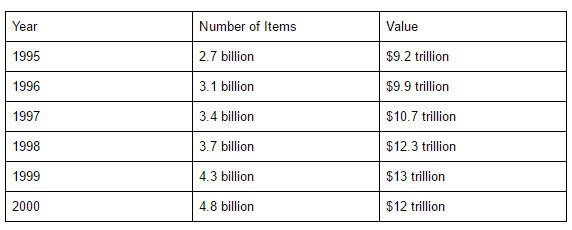

Going back a bit further in history to the time period 1995 – 2000, a steady, stratospheric rise in ACH transactions shows the need for the modern ACH system that was developed in the 1990s, and the need for dramatically increased transaction speed that came in late 2016.

ACH Items Sent to the Federal Reserve

Over the five-year time period, the number of items processed grew by an average of 420,000 per year, with the biggest jump happening between 1998 and 1999 ($600 million). The value of items processed annually increased by an average of $500.6 million in the same time period, with the largest increase coming between 1996 and 1997 ($800 million).

Over the five-year time period, the number of items processed grew by an average of 420,000 per year, with the biggest jump happening between 1998 and 1999 ($600 million). The value of items processed annually increased by an average of $500.6 million in the same time period, with the largest increase coming between 1996 and 1997 ($800 million).

Information Technology 1990s Style

The introduction of faster ACH processing services in 2016 marked the first year such a game changing improvement was made to the network since 1996, when “[the] Federal Reserve mandated that all ACH payment files would have to be deposited electronically and all output files would be delivered electronically” — an expected development in the evolution of the new, ubiquitous processing system the Federal Reserve envisioned in the mid 1970s.

The most recent upgrade to processing speed was understandably a long time coming. The IT infrastructure for payments and ACH processing services required comprehensive upgrades, which retail banks performed while overseeing the hustle and bustle of everyday business that underpinned the need for expedited payment processing.

On September 23, 2016, all the hard work and millions in investment capital paid off. Prior to just over a year ago, the ACH system processed payment requests once a day, usually overnight when most businesses were shuttered for the evening. Retailers that accept ACH payments online had to wait about three days for cash to transfer and provide payment.

On September 23, 2016, all the hard work and millions in investment capital paid off. Prior to just over a year ago, the ACH system processed payment requests once a day, usually overnight when most businesses were shuttered for the evening. Retailers that accept ACH payments online had to wait about three days for cash to transfer and provide payment.

This is why online bill payments once needed to be scheduled three days in advance of the due date, and why money transferred from PayPal to a bank account took about 72 hours to show up in checking or savings. Today, whether you accept ACH payments online, in-store, or both, you can expect transfers to be originated and closed on the same day. NACHA notes the following recommended “clearing windows” during which payment can be presented and cleared:

- A morning submission deadline at 10:30 AM ET, with settlement at 1:00 p.m.

- An afternoon submission deadline of 2:45 PM ET, with settlement at 5:00 p.m.

Because payments are processed in batches, businesses can clear exponentially more revenue in a single day than they could have as recently as the middle of last year. Since payments occur faster, consumers get the benefit of viewing account balances in real-time, which helps them avoid shopping with money that isn’t really there, thus helping them avoid a string of insufficient funds fees that run about $35 for each insufficient funds purchase.

How the New Processing System Works

Processing services for ACH transfers may be faster than ever, but they still involve the same parties — originator, originating depository financial institution (ODFI), ACH operators (the Federal Reserve or the Clearing House), Receiving Depository Financial Institution (RDFI) and recipient — as well as a similar fee structure: same day fees, account fees, credit payment fees, debit payment fees, and discount fees.

According to the NACHA, “Businesses and consumers [can] benefit from same-day processing. [The payments] enable ACH Originators that desire same-day processing the option to send same-day ACH transactions to accounts at any receiving depository financial institution. The Rule includes a ‘same day fee’ on each Same Day ACH transaction so that RDFIs would recover, on average, their costs for enabling and supporting Same Day ACH.”

So, for just an additional, small fee — the same day fee — businesses and consumers can make ACH payments that are settled on the same day. But there’s an exception: “International transactions (IATs) and high-value transactions over $25,000 will not be eligible.” However, as NACHA points out, “Eligible transactions account for approximately 99 percent of current ACH Network volume.”

ACH Payment Services Upgrades

There are major upgrades to the ACH payment process that are pushing ACH transactions into a future, where speed is vitally important: more ACH payments batch processed daily.

More ACH Payments Processed Daily

Largely responsible for making same-day transfers possible is increased ACH payment processing frequency. Instead of performing those once a day, batch-processed transfers under the cover of darkness, the network now has the capacity to process payments a minimum of three times a day.

Right off the bat, the change benefits consumers by giving them more purchasing power, and thus benefits businesses in three primary ways: increased revenue flow, higher corporate cash balances, and avoiding the cost and hassle of “insufficient funds” transactions that receive their status days after the purchase is made.

The addition of same day fees, plus a higher frequency of account fees, credit payment fees, debit payment fees, and discount fees that result from faster ACH processing benefits the Federal Reserve and, by extension, the U.S. Treasury. As it looks right now, after having observed the new processing protocols for over a year, faster ACH processing services benefit everyone involved.

Impact on Consumers and Businesses

For consumers, the biggest benefits of the upgrades are the ability to move money between accounts with greater speed (which supports faster consumer crediting), faster automatic paycheck deposits, and expedited bill payment, which, according to NACHA, “[enables] consumers to [use ACH debits and credits to] make on-time bill payments on due dates, and provide faster crediting for late payments.”

For consumers, the biggest benefits of the upgrades are the ability to move money between accounts with greater speed (which supports faster consumer crediting), faster automatic paycheck deposits, and expedited bill payment, which, according to NACHA, “[enables] consumers to [use ACH debits and credits to] make on-time bill payments on due dates, and provide faster crediting for late payments.”

For businesses, there are three benefits to cite, too, in addition to the benefits of increased revenue flow, higher cash balances, faster delivery of purchases, and avoiding insufficient funds transactions: same-day payrolls that support compensation for hourly workers, provide payment flexibility for late payrolls, facilitate quicker business-to-business (B2B) payments that support faster invoice settlement, and financial predictions based on real-time finances that don’t include payments hanging in the balance.

For businesses, though, perhaps the greatest advantage hasn’t been mentioned yet: They don’t need to build a comprehensive, new IT infrastructure to take advantage of the aforementioned benefits. Rather, the benefits kick in automatically for businesses that perform transactions through entities that have made the upgrades.

If you operate a business that has a merchant account for ACH payment services and accepts payments through major, third-party payment processing services, or if you manage a financial institution that accepts transfers from processing services, you’re in a great position to take advantage of ACH payment services upgrades that are changing how we transfer money, receive transfers, and make electronic payments.

About Our Company

Allied Wallet is a global merchant service provider (MSP) that offers notable benefits to merchants of all sizes, including encrypted transactions, 164 currencies accepted from 196 countries, novel chargeback prevention features, and offshore credit card processing solutions, just to name a few. As a testament to our dedication to service, we’ve been featured in TIME, Forbes, Fortune, The Wall Street Journal, and other respected publications.

Need a New Account?

If so, it’s easy. To open a merchant account or inquire about our ACH payment services, simply call us in the U.S. at (888) 255-1137, give us a call in the U.K. at +44 203 318 8334, or send us an email through our contact form. We look forward to learning about your ACH payment services needs and seeing how we can help you leverage the latest technologies.